E2E implementation of UPI (Unified Payments Interface)

April 30, 2024

The environment of digital payments has significantly changed in recent years, revolutionising how consumers send and receive money as well as how they make purchases. The Unified Payments Interface (UPI has become extremely popular in India, is one such ground-breaking innovation. In addition to streamlining transactions, UPI has promoted financial inclusion and economic expansion. India logged more digital payment transactions last year than the combined total from the US, China, and Europe [1].

Unified Payments Interface (UPI) is a real-time payment system introduced by the National Payments Corporation of India (NPCI) about seven years ago on April 11, 2016. It allows users to link multiple bank accounts to a single mobile application and make seamless peer-to-peer (P2P) and peer-to-merchant (P2M) transactions. UPI leverages the existing infrastructure of banks and enables secure, instant, and convenient fund transfers using smartphones. The number of UPI transactions keeps increasing month after month, surpassing the previous month’s total. According to the NPCI, for the month of June 2023, the total number of monthly UPI transactions reached a record 9.3 billion with the transaction value of record INR 14.75 trillion (about USD 179 billion) [2].

India has taken a lot of initiatives to expand UPI’s usage beyond its borders and make it a genuinely global payment system. The Indian and national initiatives for cross-border and global UPI payment services are detailed below.

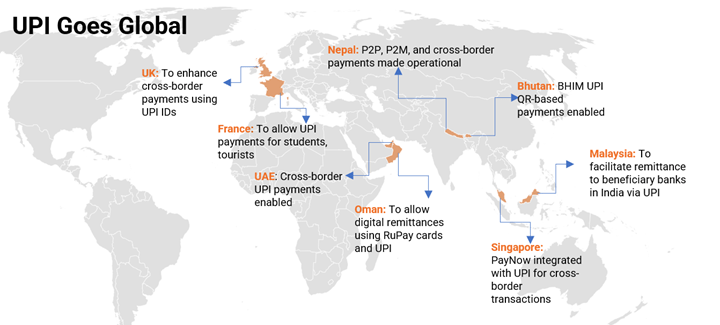

Unified Payments Interface Goes Global

The Reserve Bank of India (RBI) established NPCI as a non-profit umbrella organisation to manage India’s retail payment and settlement systems. NPCI has undertaken several initiatives to make it possible for UPI to be used internationally for peer-to-peer and merchant payments. NPCI mandated all its stakeholder/ member banks, Payment Service Providers (PSPs), and Third-Party Applications to enable the international merchant payments on UPI by 31st Dec 2021[3]. To accommodate new members who had not yet implemented the feature at the issuer and UPI app level, this deadline was extended to 30th September 2022[4] however, NPCI has not given any other extensions. The first Indian fintech to launch cross-border UPI payments was PhonePe. Users of PhonePe can make payments to merchants at points of sale or merchant outlets in the UAE, Singapore, Mauritius, Nepal, and Bhutan using their Indian bank accounts [5].

NPCI has allowed Non-Resident External (NRE) and Non-Resident Ordinary (NRO) accounts with international mobile numbers to use UPI and granted permission for mobile number from 10 countries – Singapore, Australia, Canada, Hong Kong, Oman, Qatar, USA, Saudi Arabia, United Arab Emirates and United Kingdom. The Member banks are responsible for adhering to RBI regulations and FEMA (Foreign Exchange Management Act) guidelines. While remitter and beneficiary banks are accountable for adhering to AML (Anti-Money Laundering) and CFT (Combating of Financing of Terrorism) compliance validation [6].

Countries like UK, Singapore, and UAE have partnered with India’s NPCI through its fully owned subsidiary NIPL (NPCI International Payments Limited). This collaboration aims to provide frictionless cross-border payments, enabling Indians to use UPI in Singapore for both peer-to-peer and merchant transactions as well as in the UK and UAE for peer-to-merchant transactions. NIPL has its sights set on collaborations with major international private fintech businesses. It collaborated with TerraPay, a provider of international real-time payments infrastructure, by signing an MOU that will enable Indian citizens having a UPI ID to use TerraPay for real-time overseas payments [7].

NPCI is now attempting to make cross-border transactions possible with several other nations. It intends to work with at least 30 additional nations, including Australia and France. Many developing nations stand to gain from the remarkably cheap prices and safe method for conducting UPI-based digital transactions, as they strive to build the digital financial infrastructure necessary to create a globally integrated digital economy [8].

Exhibit 1: Key implications of Web 3.0

End-to-End Implementation of UPI:

Implementing end-to-end cross-border UPI (Unified Payments Interface) transactions requires a robust architecture that integrates various components and systems. Below are the steps to follow for implementing cross-border UPI transactions:

User Interface (UI) Layer: Users can start and manage cross-border UPI transactions using a mobile application or web interface. For transaction initiation, currency selection, beneficiary administration, and transaction history, the programme must have an intuitive user interface.

Authentication and Authorization: To enable safe access to the programme, user authentication methods like biometrics, PIN (Personal Identification Number), or passwords are implemented. Systems for authorising transactions that verify user rights and transaction caps.

API (Application Programming Interfaces) Gateway: Integration with the member nations’ UPI infrastructure. APIs (Application Programming Interfaces) for sending and receiving UPI transactions across borders. Secure communication protocols (HTTPS) and encryption are used to protect sensitive data during transmission. serves as a single point of entry for controlling incoming API requests. provides request/response transformations, rate restriction, and authentication. assigns the relevant internal services to manage the request.

User Verification and KYC (Know Your Customer): Verification services to confirm user identities and guarantee KYC standards are being met. Integration with systems that enable identity verification, such as Aadhaar or other national identification programmes. verification of the bank account information that the user has submitted and the related KYC records.

Currency Conversion: Real-time exchange rates are provided by integration with currency conversion services or forex platforms. Based on the chosen currencies, conversion logic can compute and display precise converted values.

Transaction Routing and Switching: Determines the best route for international UPI transactions. Enables secure transaction routes by establishing connections with partner banks and payment service providers. Controls switching transactions between various systems and the UPI infrastructure.

Settlement and Reconciliation: Payment service providers and collaborating banks can transfer payments via settlement systems. Mechanisms for reconciliation to guarantee correct recording and reporting of international transactions. Integration with payment networks, including neighbourhood clearinghouses or correspondent banks.

Fraud Detection and Risk Management: Implementing fraud detection techniques will help to spot unusual activity and stop fraudulent transactions. Detecting anomalies through real-time analysis of user activity, transaction patterns, and transaction amounts. integration with risk scoring and risk mitigation decision engines and risk assessment systems.

Compliance and Security: Security mechanisms, such as tokenization, encryption, and secure communication protocols, are put into practise. Adherence to local data privacy laws or data protection rules like the GDPR (General Data Protection Regulation). Anti-money laundering (AML) standards and adherence to international financial legislation.

Reporting and Analytics: Creation of statistics and reports on user behaviour, trends, and transaction volumes. Evaluate system performance and user satisfaction, key performance indicators (KPIs) are monitored. Integration with analytics tools for corporate insight and data visualisation.

External Integrations: Integration with external systems, including payment gateways, regulatory agencies, and banking partners. For smooth integration, these systems can communicate data through APIs and webhooks.

Infrastructure and Scalability: Deployment of a durable, scalable infrastructure that can manage large volumes of transactions and guarantee system availability. Horizontal scaling, caching, and load balancing are used to meet rising user demands.

Benefits of E2E Implementation of UPI:

The benefits of UPI payments that improves the customer’s digital payment experience are listed below.

Instant transactions: Users can start making payments instantly following a brief registration process. UPI transactions are by nature immediate. Within seconds, they appear in the recipient’s account. As a result, UPI is a time-saving payment method that enables users to conduct low- and high-value payment transactions. The daily transaction cap is determined by the cap set by the UPI platform and the UPI platform-affiliated bank.

Promotes a cashless economy: UPI has revolutionised digital payments by enabling peer-to-peer, merchant, and interbank transfers. It enables users to conduct numerous financial transactions that take place every day. Users do not need to worry about having cash because transactions are managed digitally. The cashless system further reduces the possibility of losing actual cash.

Simplified Payments: By removing the need to disclose bank account information or go through numerous authentication processes, UPI streamlines the payment process. Users can initiate transactions using their distinctive UPI ID or by scanning a QR (Quick Response) code, which simplifies the payment process.

Enhanced Security: UPI transactions are safe and secure from potential security risks because to end-to-end encryption and secure authentication techniques. A further degree of security is provided using UPI PINs (Personal Identification Number) and device-based authentication.

Merchant Benefits: UPI adoption for enterprises enables speedy settlement of cash into their bank accounts. The availability of UPI QR codes also decreases the requirement for point-of-sale (POS) hardware, making it simpler and more affordable for small businesses to accept digital payments.

Challenges of E2E Implementation of UPI:

Some of the major challenges of UPI’s E2E implementation were:

Regulatory requirements: National Payments Corporation of India (NPCI) and the Reserve Bank of India (RBI) have published tight regulatory standards that must be followed when implementing UPI. It might be challenging to ensure compliance with these rules while creating a fluid and user-friendly experience. It might be time consuming and difficult to follow the rigorous rules and acquire the required licences, especially for new entrants to the payments sector.

Digital literacy: The UPI system is inaccessible to most people since they are digitally illiterate. Digital payment systems may not be well understood by many users, which could result in mistakes, misunderstandings, and security problems. Increase UPI usage and reduce potential hazards, it is essential to educate users on the technology, its benefits, and safe practises.

Cross-Border transactions: Due to regional regulatory and technological variations, extending UPI to facilitate cross-border transactions or opening it up to international users may provide extra difficulties. Along with RBI and NCPI guidelines such as FEMA (Foreign Exchange Management Act) needs to be followed strictly while enabling cross-border transaction in UPI.

Integration process: Integration with numerous stakeholders, such as banks, payment service providers (PSPs), and the National Payments Corporation of India (NPCI), is necessary for the implementation of UPI. Integration may be difficult and time-consuming because each organisation may have unique APIs, security procedures, and documentation. It might be difficult to ensure effective communication between all concerned parties.

Changes in Guidelines: Due to the rapid evolution in UPI ecosystem’s, NPCI’s guidelines may occasionally alter. For companies and service providers, it can be difficult to adapt to these changes and maintain compliance.

How Brickendon can help?

Brickendon can analyse the existing payment infrastructure of any company and can evaluate how UPI can improve their customer experience.

We can assist in understanding and complying to the regulations and guidelines set by RBI and NPCI.

Brickendon can help in establishing and integrating API connections and ensuring effective communication with all parties such as NPCI, banks, PSPs, forex.

Brickendon can help in implementing strong security measures to protect user data with features like encryption, two-factor authentication, biometric authentication.

We can help in the development of user manuals, frequently asked questions, and customer service procedures to aid users in understanding and using UPI.

Let us help you prepare for the coming changes

Explore the latest Insights from Brickendon and ensure that your organisation is prepared.