The multitude of costs and risks faced by banks in their OTC derivatives trading operations – outside the typical risks of a Trading Book – have led to the adoption of various xVAs, (‘valuation adjustments’) aiming to bridge the gap between fair and actual value. Practitioners often refer to these VAs as ‘components’ of the Accounting-xVA, the amount ‘chargeable’ to the counterparty in theory, and/or to be reserved for the potential risks.

Whilst calculation of the adjustments are valuable – essential for a large and diverse investment bank- as they bring greater awareness and clarity to the multitude of risks and costs when managing a derivatives operation, efficient adoption of xVAs presents its own difficulties – to name a few: combining or centralising xVA trading operations within the investment bank, developing complex IT infrastructure encompassing modelling and trade/market-data requirements, dynamic risk management & controls.

Slightly distinct from accounting xVA, touched on above, is its regulatory counterpart. Regulators demand that investment banks hold capital against the volatility in the CVA exposure, to ensure resilience in the face of losses. From 2023, at a yet-to-be-agreed time frame, regulators expect calculation of the Reg-CVA to occur through the ‘Basic Approach’ or ‘Standardised Approach’ CVA methodologies, in line with the adoption of the wider FRTB framework thus sharing many aspects on risk-identification and quantification. This is a major change in the CVA regulatory space; departing from the ‘current’ Basel III standardized-CVA-approach to a more complex, but pragmatic approach (SA-CVA) requires careful understanding of the regulation, which, if synchronised with the use of a dynamic accounting-xVA approach, will allow investment banks to minimise this capital commitment, freeing up costly capital in the process.

The proliferation of the xVA concept in derivatives trading provides new opportunities by allowing trading businesses to better understand and manage the multiple costs of their derivative book, analyse the capital efficiency of specific businesses or trading activities, as well as the cost of entering and/or exiting complex trades. Active calculation and monitoring must be combined with prudent and dynamic risk management. Given that the xVA, by design, spans across all asset classes and almost the complete trade type and population of a derivative book, ensuring that an upgraded and suitable IT infrastructure is in place becomes pivotal. Successfully embedding the xVA process is primarily an IT and Quantitative Modelling exercise; significant benefits will be found, for allowing rapid calculation of xVAs for pre-trade assessment, dynamic risk reporting for hedging, and synergies with the Regulatory CVA calculation process.

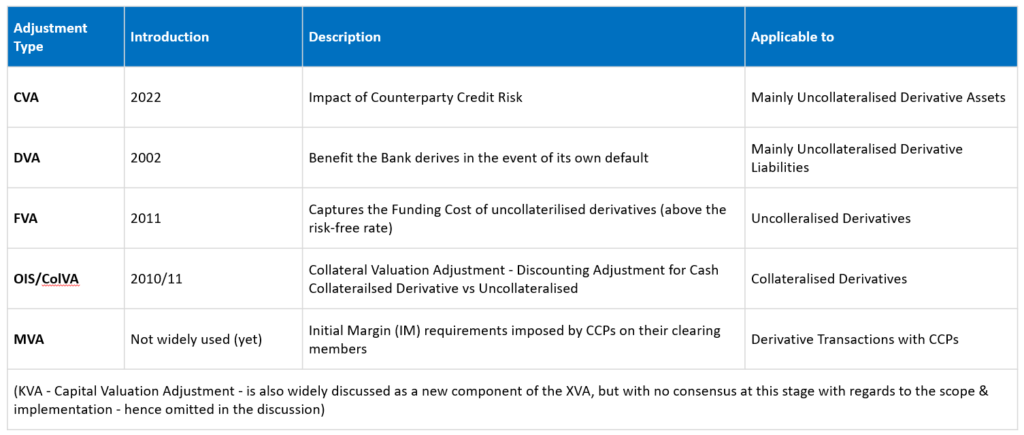

‘Mainstream’ xVAs – CVA, DVA, FVA, ColVA

As it stands, the xVA landscape is dominated by the Credit Value Adjustment (CVA) and DVA, these being the most widely implemented and used of value adjustments. CVA is the most ‘basic’ adjustment banks consider, reflecting the cost of replacing the hedge-trade(s) of a derivative book in the event that the counterparty defaults. Other realities of the post-crisis world, such as changes in bank funding costs, the emergence of new basis-risks in interest rates (eg LIBOR/OIS) and the increasing movement towards collateralisation, drove the emergence of other adjustments such as the Funding (FVA) and Collateral (ColVA) Valuation Adjustments.

This paper will lay out the challenges and complexities involved in designing, constructing and implementing an xVA infrastructure, with an eye towards both regulatory compliance and prudent risk management.

The emergence of accounting CVA as a commonplace adjustment to OTC derivatives has introduced a new source of PnL volatility to a banks trading businesses – changes in counterparty creditworthiness and exposures can bring about sharp and unexpected loses. This has motivated regulators to mandate fresh capital requirements to offset this CVA-driven volatility, introducing a compliance angle to the XVA landscape while, indirectly, incentivizing banks to transact more on a collateralized-basis (eg via clearing houses).

Whereas there is some argument about the scope and methodology concerning accounting xVAs, regulatory CVA represents the implementation of local regulator/supervisory requirements. As banks are asked to transition from the Basel III (std-CVA currently in place) framework into the new one (FRTB aligned) sometime in 2024, the adoption of Basel IV CVA regulation poses fresh challenges to trading businesses over the implementation; banks will face a choice in methodology for calculating their CVA capital charge, a decision that, if optimised and executed in parallel with a dynamic accounting xVA pricing and risk-management, can bring about sizeable capital savings. The regulatory options for a trading business, in increasing levels of sophistication, are:

For sophisticated investment banks, the SA-CVA methodology ensures that regulatory CVA is more closely attuned to its accounting counterpart; this means that risk sensitivities and CVA PnL will be more synchronised across the two areas. Such synchronicity resolves both operational difficulties around internally reconciling the two concepts along with bringing about a better, and often lower, RWA profile through the careful pricing and dynamic managing of accounting xVAs.

In spite of this, the substantial cost of implementing the SA methodology, both in terms of head-count resources and risk & QA/IT infrastructure, makes the decision to adopt the framework more complex, especially for firms on the margin in terms of hedging sophistication as well as size of their derivative book. For instance, a banks SA-CVA model will require careful calibration, back-testing, dedicated controls & oversight and ultimately regulatory scrutiny & approval – a process that if implemented sub-optimally can result in smaller RWA savings, and/or prolonged completion period with escalated costs.

But we do feel that firms should not be deterred by the complex implementation and analyse the overall benefits that BA versus SA CVA will bring in terms of capital (RWAs), always in relation to the product type and/or type of business dominating the banks derivative book. As a secondary consideration we note that the regulatory frameworks almost always expand in future to cover newer risks or enhance methodologies, especially for “less mature” risk types (as the CVA), and therefore delaying the adoption of the complex version (SA CVA) might come at a cost if “forced” (additional) requirements are to be rolled out in years to come.

The origins of xVA stem from the desire to ensure a systematic pricing methodology for various costs and risks borne by derivatives dealers. As already mentioned, this desire was accelerated by the financial crisis and the seismic effect it had on the OTC derivatives market; more specifically:

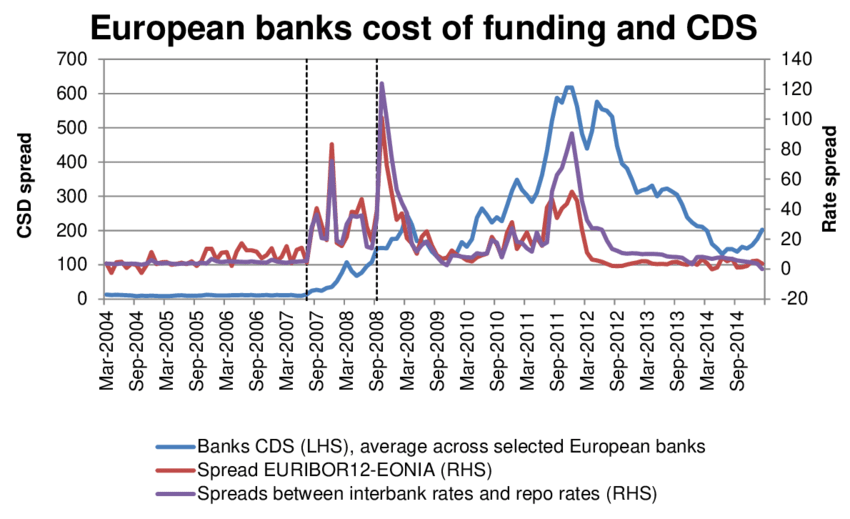

Comments on Chart:

1. Bank funding costs represented by the Credit-Default-Swap – note the negligible cost level level pre-07 and subsequent volatility.

2. The 2008 Fin-Crisis impacted the way we view Rates – note the rate diff between EURIBOR & EONIA – almost zero pre-07 and note subsequent divergence, which tends to increase in periods of stress – impacts the calculation of the ColVA.

The rising cost pressures in dealing OTC derivatives in the post-crisis landscape incentivised investment banks to increasingly calculate and risk-manage these xVAs, both in order to assess their own costs and risks and to ensure more competitive pricing and deal-making. The widespread adoption of fast computational techniques also facilitated this adoption, allowing for rapid calculation and dissemination of xVAs and their associated sensitives.

Accounting xVA & Risk Management

The careful monitoring and managing of xVA is of vital importance for a bank active in derivatives trading both from a risk management and competition perspective. Larger and more sophisticated institutions will likely see benefits from running a dedicated xVA trading desk under clear pricing & trading mandates covering the totality of the business units, rather than ‘in-business’ xVA adjustment performed selectively.

It will be totally understandable if small/mid-sized banks take a less proactive approach to xVA, however, even for smaller banks, a keen awareness and frequent calculation of their xVA exposure is still of paramount importance. Market volatility can cause an initially innocuous xVA exposure to bring about significant loses, especially if market dislocations persist. Or it may well be the case that overtime, the current dominant business model or trade strategy evolves slowly into a ‘high-CVA’ risk-profile, with trades of longer maturity, different strike-prices or more volatile-risk-factors.

Beyond these risk management issues, the rapid proliferation of xVAs has created an environment which severely lacks uniformity. Throughout the industry, there is no established protocol for dealing with potential overlaps emerging from xVAs – how to split, account and hedge the CVA/DVA/FFVA components. For example, the overlap between DVA and FVA – in terms of the benefit to the firm from having a negative MtM on some positions – has led to some firms dropping DVA all together. Such issues highlight the risks that a lack of homogeneity brings to the firm, as an inconsistent application of xVAs prevents a firm from being able to compare costs across trading desks and from systematically charging clients for these costs.

While methodologies for calculating funding & credit-risk are well established, with MVA & reg-capital cost still evolving, blending their respective cost into a single ‘unwind-cost’ is a challenge with no apparent consensus among banks. Ultimately accounting decisions on the weighted contributions of the main xVA components does impact, first and foremost, hedging and P&L volatility, and secondly the charge banks apply on new or unwind trades.

xVA Activity – Concluding Remark

Our experience guides us towards supporting a centralised xVA activity – a single service-provider desk covering all asset class business – without opt-outs and exceptions, operating on agreed product/payoff cover with transparent and consistent pricing methodology reflecting hedging costs and the banks credit risk appetite. Such centralisation drives more uniformity in determining which costs are passed on to counterparties when executing or unwinding trades. A central xVA utility function may be fulfilling a number of roles, depending on the sophistication of the banks:

or

[1] Hałaj, G. & Henry, J., Sketching a roadmap for Systemic Liquidity Stress Tests (SLST) (draft, final version in Journal of Risk Management in Financial Institutions. ResearchGate. Available at: https://www.researchgate.net/publication/328047996_Sketching_a_roadmap_for_Systemic_Liquidity_Stress_Tests_SLST_draft_final_version_in_Journal_of_Risk_Management_in_Financial_Institutions [Accessed September 20, 2022].

Explore the latest Insights from Brickendon and ensure that your organisation is prepared.